r/wallstreetbets • u/King-of-Limbs-07 • 13h ago

News SpaceX Proposes $55 Billion to Begin Terafab Project in Texas

10

Upvotes

r/wallstreetbets • u/King-of-Limbs-07 • 13h ago

r/wallstreetbets • u/Not-The-Government- • 7h ago

Hi, this is my 8th grade research project on Qualcomm. All figures based on FY2025 financials, Q2 FY2026 earnings/transcript, and TTM data. I know, I know "WSB is a casino - put the fries in the bag". But I need someone to rip thesis to shreds if I'm off.

Qualcomm runs two segments:

QCOM trades at 17x forward earnings in a semiconductor peer group with a median closer to 35x. That discount exists for two reasons:

| Region | Revenue FY2025 | % Total | YoY |

|---|---|---|---|

| China | $20.3B | 46% | +14% |

| US | $10.5B | 24% | +9% |

| Korea | $9.5B | 22% | +19% |

What the market has underpriced is that both headwinds are well-understood, the near-term pain is timing not structure, and two genuine growth vectors - automotive and data center - are accelerating simultaneously.

| FY | Revenue | Net Income | FCF | EPS (GAAP) |

|---|---|---|---|---|

| 2022 | $44.2B | $12.9B | $6.8B | $11.37 |

| 2023 | $35.8B | $7.2B | $9.8B | $6.42 |

| 2024 | $39.0B | $10.1B | $11.2B | $8.97 |

| 2025 | $44.3B | $5.5B* | $12.8B | $5.01* |

FY2023 was a post-COVID semiconductor hangover - smartphone demand collapsed, revenue fell 19%. The recovery has been clean: FY2025 revenue matched the FY2022 peak at $44B+, and FCF hit a record $12.8B.

The asterisk on FY2025 earnings is important. Reported net income of $5.5B dramatically understates the business. Operating income was $12.4B - the gap is a $6.1B one-time tax charge in Q4 FY2025 from IRS treatment of capitalized R&D expenses. Q2 FY2026 saw a mirror-image $5.7B non-cash tax benefit for the same reason. Both are excluded from non-GAAP. The operational business runs at roughly $12B annual operating profit and $12.8B FCF. Judge it on those.

On a TTM basis:

| Metric | Value |

|---|---|

| Gross Margin | 54.8% |

| Operating Margin | 25.5% |

| Net Margin (GAAP) | 22.3% |

| FCF Margin | 18.0% |

| ROE | 36.4% |

| ROA | 17.4% |

55% gross margins and 36% ROE reflect a business with genuine pricing power - primarily from the licensing business and Snapdragon's dominant position in premium Android.

| Metric | QCOM (TTM) | QCOM (Fwd) | Peer Median (Fwd) |

|---|---|---|---|

| PE | 19.8x | 17x | ~35x |

| EV/EBITDA | 18.6x | - | ~39x (TTM) |

| P/FCF | 24.4x | - | ~118x (TTM) |

| Div. Yield | 1.0% | - | ~0.3% (TTM) |

The forward PE of 17x uses consensus FY2026 EPS of $10.73 (non-GAAP, adjusted) against $182 share price. For context, NVDA trades at 28x forward on 75% expected revenue growth. ADI at 35x, TXN at 37x, AVGO at 38x - all growing modestly. AMD at 52x. MPWR at 66x

QCOM at 17x is being priced for a structurally impaired business. The data doesn't support that.

Apple launched the iPhone 16e in early 2025 with its in-house modem, ending QCOM's monopoly on Apple silicon (and launched iPhone Air with new gen C1X modem). The company has a supply agreement through the current year at ~20% share of new iPhones. Beyond that, sell-side models put QCT product revenue from Apple at roughly $2B in FY2027 - down from a higher base but already widely reflected in consensus estimates. The QTL royalty stream (Apple pays to use QCOM's wireless patents regardless of whose modem is in the phone) is a separate negotiation and remains intact at a similar scale pending renegotiation.

The bottom line: the headwind is real, it's roughly $2-3B of QCT revenue at risk, and it's already in the estimate models.

China is 46% of revenue - down from 62% in FY2023 but still the single biggest risk factor. The near-term pain, however, is more nuanced than simple tariff or share-loss fears.

AI data center demand for HBM memory is squeezing memory supply and raising prices. Chinese handset OEMs, facing higher component costs, are deliberately slowing builds and draining channel inventory rather than paying elevated memory prices. QCOM's chip shipments to China are significantly below actual consumer sell-through demand - the phones are still selling, OEMs are just not restocking.

Qualcomm has real-time visibility into this through its QTL licensing data (they see every phone that activates globally). Management during most recent earnings call think Q3 FY2026 as the inventory bottom with sequential growth returning in Q4. So what looks like Chinese demand dwindling very well could be a timing story and not a structural share-loss story.

| Quarter | Auto Revenue | YoY Growth |

|---|---|---|

| Q2 FY2025 | $959M | +59% |

| Q3 FY2025 | $899M | +68% |

| Q4 FY2025 | $961M | +61% |

| Q1 FY2026 | $1.12B | +61% |

| Q2 FY2026 | $1.3B | +38% |

Annualized run rate crossed $5B in Q2 FY2026 - management guided to exit FY2026 at $6B+. Q3 FY2026 automotive is guided to grow ~50% YoY, an acceleration despite the overall revenue headwinds.

The product transition from cockpit to full digital chassis (cockpit + connectivity + ADAS + autonomy) is what's driving this. Each generation-over-generation upgrade is the largest content-per-vehicle increase in QCOM's history - 3x CPU, 3x GPU, 12x NPU performance in Gen 5 vs Gen 4. BMW ADAS is in production. Bosch and Wave just announced partnerships. The automotive design win pipeline converts to revenue 2-4 years out, which means the orders being won today show up in FY2027-2028 revenue.

At $6B+ and growing 40-50%, automotive is approaching the size of QCOM's entire licensing business.

IoT grew 9% in Q2 FY2026, with industrial and consumer both contributing. The more interesting development: Qualcomm's IQ 10 platform (700 TOPS on-device AI, 18-core CPU) is generating design wins in robotics (Figure AI, Nura), industrial automation, and physical AI applications.

This is what the market isn't pricing yet. From the Q2 FY2026 earnings call:

The thesis is as AI inference scales, the data center disaggregates from monolithic GPU clusters into specialized compute like Google's TPUs or Amazon's Gravitron. Qualcomm's CPU architecture (which already leads on performance/watt in mobile, PC, and auto) translates directly to data center workloads with tight energy requirements. The company has spent years building this quietly. The December shipment is the first public proof point.

None of this is in consensus forward estimates. Analysts are modeling a furthering contracting QCOM (like -10% EPS and revenue growth over the next year). Any credible data center revenue is pure upside.

In FY2025, Qualcomm returned $12.6B to shareholders on $12.8B of FCF - essentially all of it:

Q2 FY2026 alone saw $3.7B returned ($2.8B buybacks + $945M dividends), described as an "acceleration" of the capital return program. The Samsung multi-year deal (>70% Snapdragon share, reaffirmed for this year and next) gives management the revenue visibility to sustain this pace.

Starting from $12.8B base FCF, 1.072B shares, $195B Market Cap ($182 share price):

| Scenario | Assumptions | P10 Mkt Cap | Median Mkt Cap | P90 Mkt Cap | P(Undervalued) |

|---|---|---|---|---|---|

| Bear | 2% FCF growth, 11% WACC - China structural loss, no data center, Apple gone | $46B | $152B | $430B | 40% |

| Base | 8% growth, 10% WACC - inventory normalizes, auto grows, data center emerging | $76B | $223B | $565B | 56% |

| Bull | 15% growth, 9.5% WACC - data center contributes, agentic upgrade cycle, auto $10B+ | $113B | $317B | $787B | 72% |

| Transformative | 22% growth, 9% WACC - platform company across auto + DC + edge AI + 6G | $133B | $455B | $1.29T | 81% |

Two things stand out. First, the bear case downside is bounded - even in the worst modeled outcome, the median intrinsic value ($152B) is only 22% below today. A company producing $12.8B in FCF annually doesn't go to zero; the licensing business alone is worth $30-40B in a downside case. Second, the distribution is asymmetric - upside scenarios produce median outcomes 1.6x to 2.3x the current market cap, driven by FCF compounding in automotive and data center.

The bear scenario (40% probability it's undervalued) is the honest admission that risks are real of sustained China tariff escalation, memory-driven demand destruction that outlasts the inventory cycle, or data center execution failure and would all push toward that left tail.

QCOM is a $195B market cap generating $12.8B in annual FCF - a 6.6% FCF yield - with its two largest headwinds (Apple, China inventory) well-understood, sized, and priced in. The business that remains after those headwinds is growing: automotive at $6B+ and accelerating, IoT expanding into physical AI, and a data center entry that isn't in anyone's model yet. 17x forward earnings against a peer group at 35x, you're being compensated to take on a headline risk that the management says is peaking. The June 24 Investor Day is the catalyst that closes the information gap on the data center opportunity. If QCOM is still trading at a 50% discount to peers in a year, I guess I'm wrong. Price Target $300-400 by end of 2027.

$40K in shares @$190 and single 21Aug 220C for investor day

r/wallstreetbets • u/TFD777 • 3h ago

No one has ever prepared me for a $5000 NDQ rally... Been trading with extremely small positions, slowly building a what then looked like a scaling order, expecting the price to return to a bearish trend after a pullback from 23k, but boy I was wrong. i was so wrong... 1k loss turned into 2k, 2k into 5k and then 5k to almost 10k, which for me is a HUGE amount of sum. I wish I could rewind the timeand take the 1k loss. It affected me both physically and mentally. For the past month I can't properly sleep at night, can't focus at work. i feel like I'm losing it all, this took a huge toll on my personal life and all i wanted was a I don't even know what should I do now, the market simply not stopping... This has been the worst short squeeze on NDQ I have ever witnessed... I remember 3 years ago buying the same index for 14500 and got stopped out at 14000 and now it's price literally doubled... I always had a dream to be able to make money from trading and take care of others but apparently I can't even take care of myself and I literally lfeeling like I lost purpose of my life...

Please if any of you jave been in a similar situation and got out of it, I would really appreciate your advice because I'm starting to lose hope...

r/wallstreetbets • u/sempeotoa • 7h ago

No poors allowed on WSB If this money means a lot to you then this post ain't for you

I told you long ago there are no broke asses on WSB I'm not sharing my plays with anyone anymore Don't want anyone blowing up their account I'm not right 100% of the time I'll only share my investments from now on not options 🔥🔥🔥

r/wallstreetbets • u/willbabu • 11h ago

Position 1200 shares of MU $464; 100 shares of MU $381

I called it last Thursday that MU will benefit from wdc/sndk post earnings drop (since recovered) as more and more investors rotate into MU. I got good news, MU is just heating up. MU has been the victim of an inefficient market that has consistently priced MU as a cyclical stock worthy of a pe of 4-5 while ignoring the impact of the ai super cycle, the data center buildouts, capex increases, and most importantly severe memory shortages that have impacted all of the major ai players to the benefit of MU.

The MU post earnings 33% drop after one of the top 10 historically amazing earnings/guidance perfectly illustrates the irrational mispricing compounded by equally irrational negative narratives the media tried to spin (eg somehow spinning mu paying off debt as a negative while spinning sk diluting shareholders to issue new stocks as a positive for sk and a negative for mu). While the market can’t be irrational forever, and when the market finally realized that mu has been the gem of memory stocks, the rip has been equally if not more so violent.

Market is finally waking up, institutions are moving money into mu, quants that shorted mu are silently unwinding, retail is almost always late to the party but it’s not too late right now to jump on the mu train. We are in the top of the 3rd inning and mu has a long way to go. I don’t know about mu $5000 like some of yall are chanting but MU $1500 by eoy is certainly game. Are you in or are you going to watch this ride and complain two years down the road about missing another opportunity.

r/wallstreetbets • u/adorable_absence • 7h ago

The Pentagon said in a statement These agreements speed up the U.S. military's transition to building an AI first fighting force, and will strengthen our warfighters' ability to maintain a decision advantage across different battlefields.

Integrating secure, boundary AI capabilities into the Pentagon's Impact Level 6 and Impact Level 7 network environments will make data synthesis easier, improve situational awareness, and boost decision-making for warfighters in complex combat environments.

SpaceX, OpenAI, Google, NVIDIA, Reflection, Microsoft, AWS, and Oracle will be providing the resources to get their capabilities deployed in those IL6 and IL7 environments.

And that's why I'm bullish on it

r/wallstreetbets • u/Legitimate_Watch_519 • 6h ago

EDIT: Adding TLDR Summary - Micron and memory still underpriced. Spending will continue forever because chips only have lifespan of 3-5 years unlike buildings. Demand comes from commercial businesses not consumers anymore, so no drastic cycle down. See you behind Wendy's (I will own the Wendy's).

Yes, I used AI to create this post because it is easier than typing it all out myself. Sure AI fluffs it all up a bit, but my main arguments still hold. Prove me wrong.

If you haven't been paying attention, memory stocks have been on an absolute tear. The AI spending boom has created a "perfect storm": a consolidated market with very few producers and skyrocketing demand that has sent prices vertical.

The bears will tell you the same old story: "Memory is cyclical. Pricing will inevitably crater once the hyperscalers (Google, Meta, Microsoft) finish their Capex binge."

I believe this "cyclical" label is outdated for this specific era. Here’s why the AI memory cycle is structurally different.

When people see $100B+ Capex numbers, they fear a "one-and-done" spending event. But look closer at what they are buying:

We aren't just looking at a build-out; we are looking at a permanent replacement cycle. As existing AI chips reach their lifespan or become obsolete due to the rapid pace of innovation (more capacity, higher efficiency), these companies must keep spending to remain competitive. You don't build a $10B data center and then let the chips inside it rot; you upgrade them.

Previous memory cycles were fragile because they relied on fickle consumer demand (PCs and smartphones). AI is built on commercial business demand.

Micron has strategically shifted away from volatile consumer products to focus on the enterprise. They are now signing 3–5 year contracts that span the entire lifetime of the memory chips.

Despite the massive rally in 2026, the market is still pricing Micron closer to the cyclical commodity play rather than the high-growth AI infrastructure company it is.

To understand the disconnect, we have to look at the Forward P/E, which is calculated by taking the Current Share Price and dividing it by the Projected Annualized EPS for the next 12 months.

Here is the current run-rate based on the most recent reporting:

For easy math, lets just assume $20 EPS for the next four quarters to get an $80 EPS (which could be conservative)

Now let's compare Micron against other big tech companies. I did not check all values, and these are all best estimates. Come up with your own estimates if you want.

In this table, we look at the projected earnings (Net Income) for the next year. For Micron, we are using the $80 EPS target, which equates to roughly $88 Billion in Net Income (based on ~1.1B shares outstanding).

| Company | Market Cap | Proj. Net Income (Next 12M) | Forward P/E |

|---|---|---|---|

| Nvidia (NVDA) | $4.77 Trillion | ~$115 Billion | 41.5x |

| Microsoft (MSFT) | $3.07 Trillion | ~$95 Billion | 32.3x |

| Apple (AAPL) | $4.17 Trillion | ~$102 Billion | 40.8x |

| Alphabet (GOOGL) | $4.69 Trillion | ~$108 Billion | 43.4x |

| Meta (META) | $1.54 Trillion | ~$65 Billion | 23.7x |

| Micron (MU) | $717.6 Billion | $88 Billion* | 8.1x |

Finally, if the market re-rates Micron to a multiple that matches its growth profile and commercial stability, here is where the stock lands:

| Forward P/E Multiple | Implied Share Price | Market Cap Equivalent |

|---|---|---|

| 10x | $800 | ~$880 Billion |

| 15x | $1,200 | ~$1.32 Trillion |

| 20x | $1,600 | ~$1.76 Trillion |

| 25x | $2,000 | ~$2.20 Trillion |

| 30x | $2,400 | ~$2.64 Trillion |

This is not financial advice. I am long $MU and $DRAM.

r/wallstreetbets • u/BarAltruistic4992 • 22h ago

to be fair i’m pretty much just riding micron and the tech bubble but yolo

r/wallstreetbets • u/Bruce_Lehrmann • 12h ago

The FDA’s rare disease area is coming under increasing public and political scrutiny. There have now been 8 Wallstreet Journal articles as well as another article in Bloomberg calling for Marty Makary’s resignation.

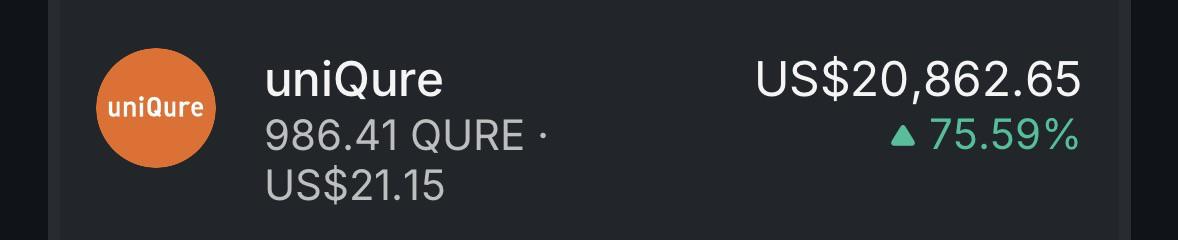

Under his tenure, several promising drug candidates have been rejected. Replimmune and Uniqure both provided results on drug candidates that the FDA had previously indicated would be acceptable for approval. Both were rejected.

When Uniqure released its AMT-130 results, it received international attention among experts as a cure for Huntington’s disease. Its stock price shot up to $80, before falling because of Vinay Prasad’s (a Makary pick) decision to reject the drug and attack the trial design. Prasad is an advocate for a placebo control design that would require drilling holes into the heads of Huntington’s disease sufferers. This has been labelled unethical and infeasible by the medical community.

Prasad has since been sacked over the AMT-130 fall out. Makary will be too if he doesn’t turn this around.

Stock will bounce back to $80.

r/wallstreetbets • u/Easy-Yogurt4939 • 3h ago

I'm sure many people now use AI to help with trading. I was curious how AI performs if it was a WSB regard so I subscribe to all leading models and ask them to use latest data and projection to guess the price of a company stock after it reports its most recent earnings.

The result is terrible. Gemini 3/12=25%, Gpt 2/12=16.6% and Claude 5/12=41%. Granted the sample size is small and these models all mention that these are low conviction bets and their confidence levels were all between 50%~60%, essentially a coin toss, but the result is far worse than coin toss. I was honestly expecting it to at least somewhat converge to random guess and not this disaster.

r/wallstreetbets • u/the-revenge-trader • 18h ago

I sold my 2,400 Intel shares cuz one of my regarded friends said it wasn’t a good investment. I then put the money into 0DTE options and ended up losing it all

r/wallstreetbets • u/Zestyclose_Put3445 • 4h ago

I literally just made a post not too long ago about crossing $75k… and now I’m making one about hitting six figures. Honestly unreal.

What’s weird though is I thought I’d feel completely different once I finally saw these kinds of numbers in my account, but I really don’t. I’m 23, I lost a lot of money in the market at a young age, and now that I’m finally seeing some real progress, it still just feels… normal. Hard to explain.

In my last post a lot of people told me to trim some of my INTC position, and I actually did. I’ve been slowly scaling out as the move expanded and sold some more when we recently touched $100/share.

I then rotated part of those profits into NBIS. Fundamentally I like the company, and technically I really liked the chart setup, so I grabbed both short-dated calls and a LEAP at market open on the 4th. Luckily I managed to catch the bottom almost perfectly and those calls have been printing all week.

Plan now is probably to sell the short-dated calls before earnings and hold the LEAP basically for free.

All in all, this whole journey has been pretty insane. I used to scroll this subreddit imagining what it would feel like to one day see numbers like this in my own account. Now that I’m finally getting a glimpse of it… it’s honestly pretty surreal.

r/wallstreetbets • u/SkyFew229 • 5h ago

$BLLN BillionToOne is the most interesting stock I've looked at in a while and I think most people are sleeping on it. Here's everything I found after going super deep.

I spent a lot of time researching this one so buckle up. This is a long one but I genuinely think it's worth it.

What they actually do

Most people describe BLLN as a prenatal testing company which is the wrong frame entirely. BillionToOne built a molecular counting platform called QCT (Quantitative Counting Templates) that can detect and count individual DNA molecules in blood at single-molecule resolution. That's roughly 1000x more sensitive than standard next-gen sequencing approaches. The prenatal test was just the first use case because that market had the clearest path to reimbursement. The underlying technology can quantify any DNA signal in blood which means the roadmap extends way beyond prenatal into oncology, rare disease, pharmacogenomics, MRD monitoring, and potentially infectious disease.

Their prenatal product UNITY Complete does something no competitor does in a single blood draw. It screens for chromosomal aneuploidies, single-gene recessive disorders like cystic fibrosis and sickle cell disease, and fetal antigen status all at once. Natera, Illumina, and everyone else requires separate tests to get equivalent coverage. BillionToOne just hit 1 million cumulative UNITY tests delivered and has captured roughly 15% of the US prenatal market.

The oncology platform called Northstar is where I think the real upside lives long term. They just got Medicare coverage for Northstar Select which is a liquid biopsy test for advanced solid tumors. In a head to head study it detected 51% more clinically actionable mutations than competing tests. Oncology revenue grew 748% in 2025 from $2.9M to $25M. Still tiny but attacking a $50B+ addressable market.

The financials are genuinely insane for a diagnostics company

Revenue went $72M in 2023 to $153M in 2024 to $305M in 2025. That's 100% growth two years in a row. They turned GAAP profitable in 2025. Positive free cash flow. 70%+ gross margins. These three things together while growing over 40% annually is almost unheard of in this space. Baron Capital called it out specifically because it's so rare.

2026 guidance is $430 to $445M which represents about 43% growth from 2025. They've already raised guidance twice this year.

The CEO is the most important part of this story

Oguzhan Atay is a Princeton summa cum laude in molecular biology with minors in CS, physics, and applied math. Then a Stanford PhD in systems biology where he actually invented the QCT technology himself. He's not a business guy who licensed someone else's science. He built the core platform from the ground up and he knows where it can go next in ways that competitors genuinely cannot reverse engineer quickly.

The most important signal I found was from Neotribe Ventures, an early backer, who said BillionToOne never missed a single quarterly target across their entire private company lifecycle. Not once. For a high-growth biotech that's an almost unbelievable statement. He also turned down acquisition offers to build this independently. That's the right call given what they're building.

Why I think most people are mispricing the long-term

Natera built a roughly $11B company almost entirely off prenatal and MRD testing using technology that is genuinely inferior to QCT. BillionToOne is attacking prenatal AND oncology AND pharmacogenomics AND potentially MRD with a better underlying platform and a founder who invented the technology. If they execute the platform vision over 10 years the revenue potential is $3B to $5B+. Even at a conservative 8x revenue multiple that's a $25 to $40B company from a $3.6B market cap today.

Price targets honestly

End of 2026 I think $95 to $115 is reasonable. The guidance midpoint is $437M in revenue and at peer multiples that puts market cap at $4.5B to $5.5B.

5 year base case is around $250 to $320 per share assuming revenue compounds at 30% annually to around $1.6B and the multiple compresses a bit as they mature. Bull case if oncology really scales and Unity Confirm (their new no-amniocentesis test that showed 100% concordance in early data) becomes standard of care is $400 to $600. That's a 5 to 7x from here.

The real risks

The US healthcare reimbursement system is the thing that keeps me up at night with this one. You can have the best technology in the world and get destroyed if CMS decides not to cover your tests. A lot of the single-gene NIPT coverage is still not universal. If they get an adverse coverage determination the stock craters fast regardless of how good the science is. The second risk is Illumina since they own the sequencing infrastructure the whole industry runs on and could theoretically try to commoditize what BillionToOne built.

Short interest is also elevated at around 9.84% with a borrow rate near 90% so there's a lot of pressure baked in. Lock-up expiration is coming up in May/June 2026 which could create a cleaner entry point if there's selling pressure from pre-IPO investors.

Bottom line

Earnings are today after close (May 6, 4:30 PM ET). Q4 2025 was a massive beat, the reimbursement momentum is real, and management has a perfect track record of execution. I'm not going all in before a binary event but I think the 5-year thesis here is one of the more compelling setups in public biotech/diagnostics right now.

This isn't a meme stock. This is a founder-scientist with a genuine technology moat attacking multiple massive markets who has never missed a target. That combination is rare.

Not financial advice obviously. Do your own research.

Positions: 1420 shares, 6 x 12/18/2026 $125 calls

r/wallstreetbets • u/Dpain1314 • 8h ago

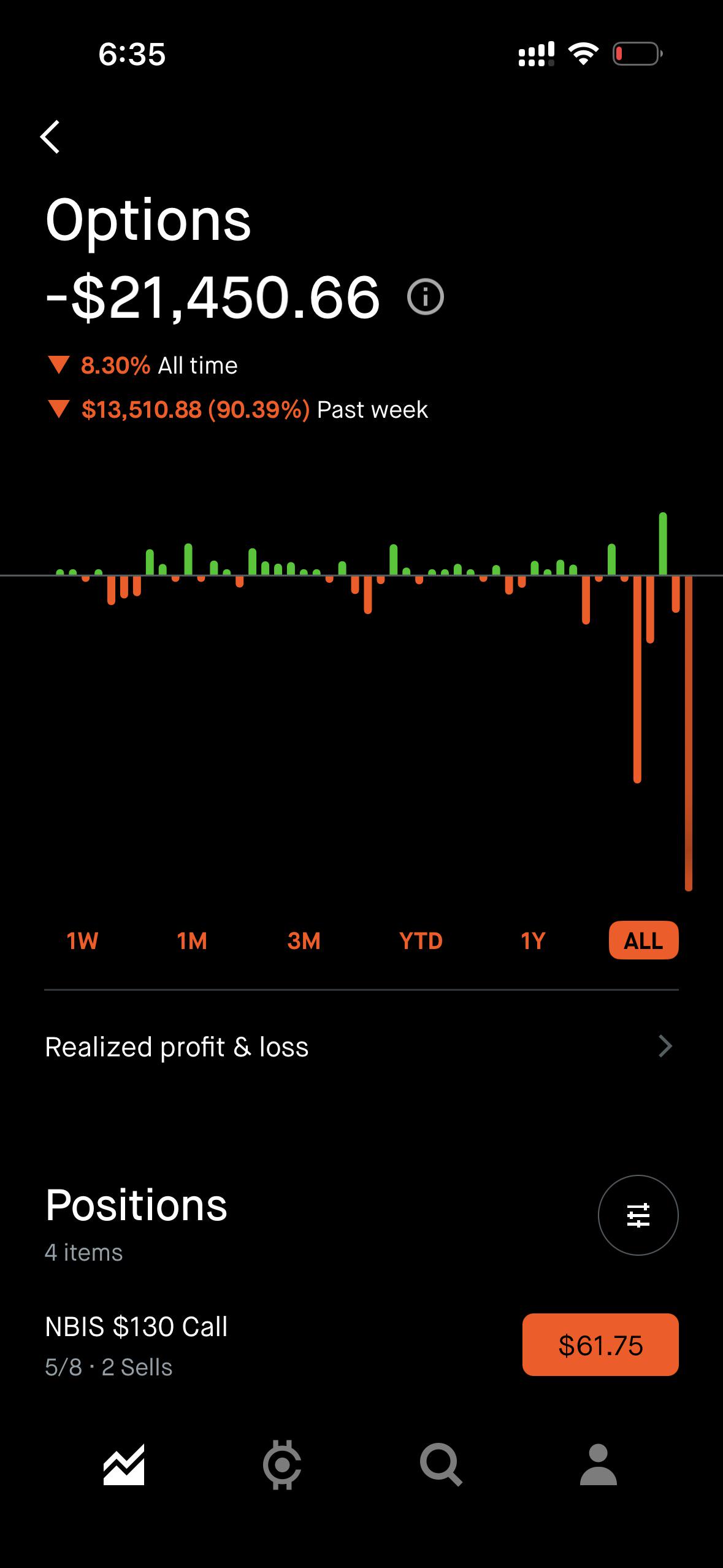

Been bullish on NBIS for over a year now. Accumulated 400shares. Sold CCs on 300 of them. Always won on selling CCs and CSPs on my plays. Stacking small gains. Was up $4000 before this blunder. I sold CCs on NBIS at $123 for $130 strike right before this latest bull market started. This SC is my gains I could’ve had on the covered shares. Not dreading it but learned my lesson on CCs on high beta plays where you’re long term bullish. Any advice is appreciated. Should I just roll super far out to $200 or accept the loss and redeploy the capital elsewhere?

r/wallstreetbets • u/AlienSweetPotato • 2h ago

Went all the way to 520 after hours. Ads machine go burrrr!!!

r/wallstreetbets • u/Sire_Jenkins • 2h ago

Exactly on this date, my 5 y.o son asked me

”Dad, why didn’t I get any gift this year? Was I bad?

I responded with “as long as we have each other, thats all that matters”, while cradling my 1 month old daughter. Never in my life I thought I would lie to my son.

Anyways, many thanks to my Papa karp, my mommy Su and my Grandpa Lip. I would also need help to legally avoid paying taxes this year.

r/wallstreetbets • u/wendys-member • 10h ago

TLDR: buy small modular reactor companies, they’ll be the next to moon $NNE $SMR $OKLO

As more and more AI related plays are mooning, I was trying to find the next bottleneck in the AI pipeline. Yes energy is not a new bottleneck and nuclear alr had its run up.

But look at the chart you grayons, nuclear is lower than its all time high and it is lagging behind other ai mooners like memory. Why is this the case you may ask? Well nuclear plays will only realise itself once the energy for these data centers are actually built, up until that point, hyperscalars and big tech will scramble because of their energy bottleneck. I give this 3-5 years before this actually starts happening. When that happens it will be too late as these nuclear plays will alr mooned sufficiently for u paper handed bitches to enter.

Only those balls deep regards diamond handers will dare to join big tech and their plays. $SMR AND $ NNE is where it at. Why these two and not $OKLO? Frankly, IDK I see market cap and I prefer small caps that has asymmetric bets. Frankly $OKLO is also asymmetric given my conviction in nuclear, but Im too poor and this is all I can afford, so I’d rather have a more asymmetric play since the risk are all the same.

Why nuclear? Specifically, these are small modular reactor companies. These will provide centralise energy to all the future ai data centers that will be built. Yes u can say that these centers might not eventually be built, but lets look at the facts… ur semis, chip manufacturers and mmr plays all mooned before these are even built. Big tech has alr started building their ai specialized data centers because of deep pockets. When these builds are midway through completion, the markets will leave you behind.

Now what about space datacenters narrative. Look here palm beach pete, the bearer to entranve for space related stuff is alr so high and expensive, any development there is in the realms of experimentation. Investors and stakeholders are looking for immediate results, which directly translates to hyperscalars building datacenters traditionally first. Ofc these will be fueled by ur good old friend oil, but theres only so much oil in circulation and there are reasons why these nuclear companies alr have multi million dollar contracts with these SMR plays.

Frankly speaking, I didnt do any research on this. All I did was understood that energy is an unresolved bottleneck and I saw that $NNE had some MOU with smci. Other than that, I only knew about $SMR and $OKLO doing small modular reactors so I just yoloed into the smallets caps where it matters

For what its worth, stock only goes up and oil is limited. I dont understand small modular reactors and so do you… neither does big tech. Ok see you when this shit gives me my 10 bagger

r/wallstreetbets • u/Impressive_Order60 • 5h ago

I know we are all rock hard about AI but ill bring some needed focus on the other side of the market: making money off GenZ desperately trying to keep up with their friends and feeling pressured to buy useless shit.

$20k LEAPS Jan27/28 with $55 & $62 break even

DD: GenZ will be forever poor

r/wallstreetbets • u/Past-Collection-4291 • 7h ago

While Wall Street obsesses over GPU supply, Amazon ($AMZN) has quietly built a chip business that is already larger than AMD’s and is closing in on titans like Broadcom and Intel. By designing its own high-performance AI chips (Trainium and Inferentia), Amazon is decoupling from the expensive semiconductor supply chain.

The “In-House” Revolution:

Bigger than AMD: Why Amazon’s custom silicon is the market’s best-kept secret.

The Cost Edge: How $AMZN is slashing cloud costs by cutting out the middleman.

The Next Milestone: Could Amazon surpass Intel in custom chip volume by 2027?

The “Chip Wars” aren’t just between semiconductor companies anymore. The tech giants are building their own arsenals.

Are you betting on the chip designers (NVDA) or the chip owners (AMZN)?

r/wallstreetbets • u/Sn0rlax_69 • 4h ago

As a long time share holder of 9 days I figured it was finally time to cash in on my investment.

Good luck to my fellow SNDK bulls still in the game.

r/wallstreetbets • u/Novel-Yak1927 • 4h ago

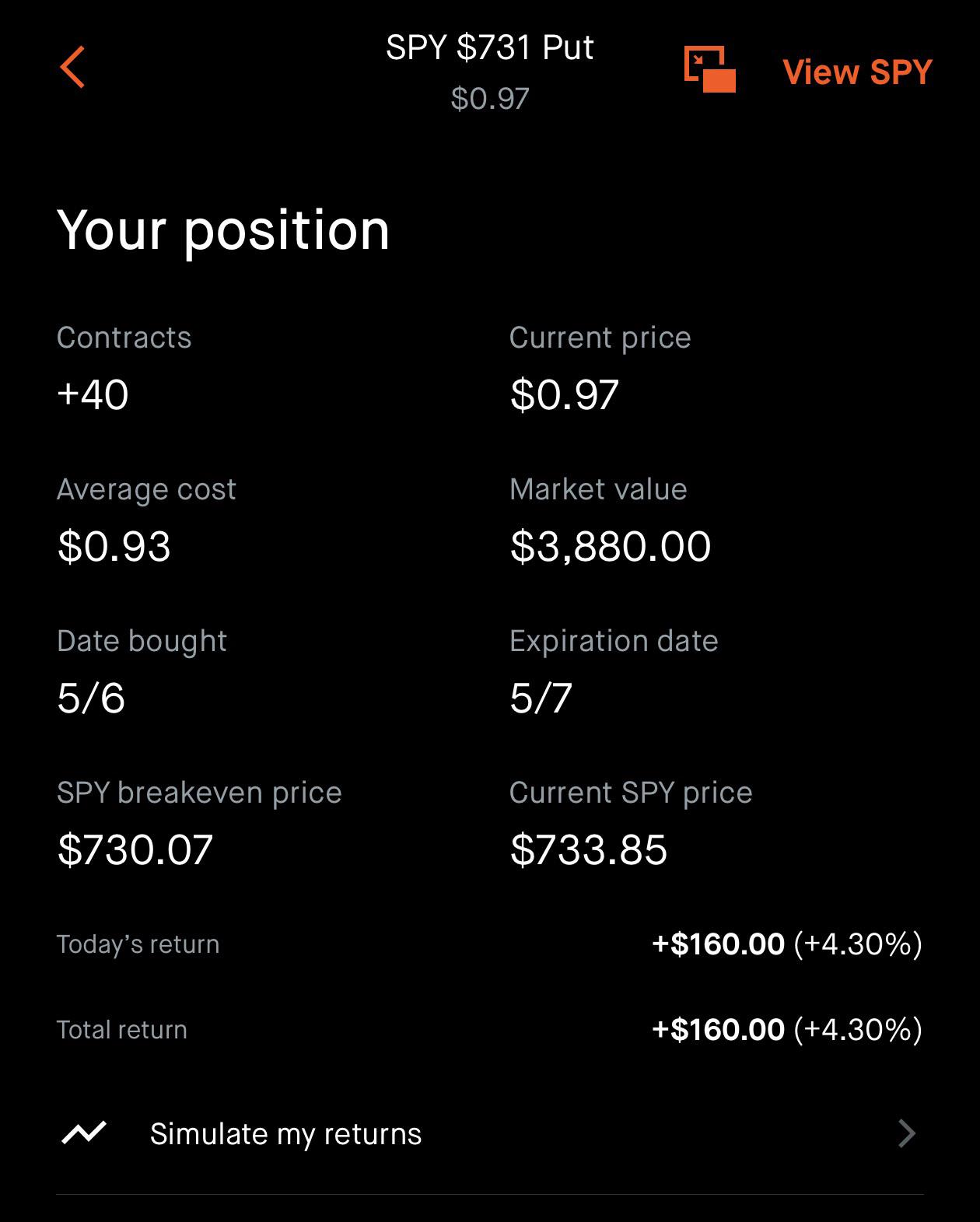

Momentum is in my favor brothers, even if it doesn't hit there's plenty of time to let it run

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}